We’ve all been in that boat at one point or another in our lives. Where the surprise bills pile up one after another. Where you look at your bank account and that small balance remaining and wonder how you will ever make it.

Let’s say you get hit with an auto repair bill for $5,000. You look at your bank account, see that it has a balance of $7,000, and tell yourself that this can be handled. You pay the repair bill.

Except that you forget you have a mortgage payment due for $1,200, a car payment of $400, and $400 going out to your child’s college savings fund.

When you take the mortgage payment, car payment, and college savings fund payment out of there at the start, that leaves you with $5,000 before the repair bill.

This is why many people run out of money before next payday.

The Tool You Need is a Budget

The greatest tool at your disposal to avoid paycheck to paycheck living is a budget. A budget is how you stop running out of money before your next paycheck.

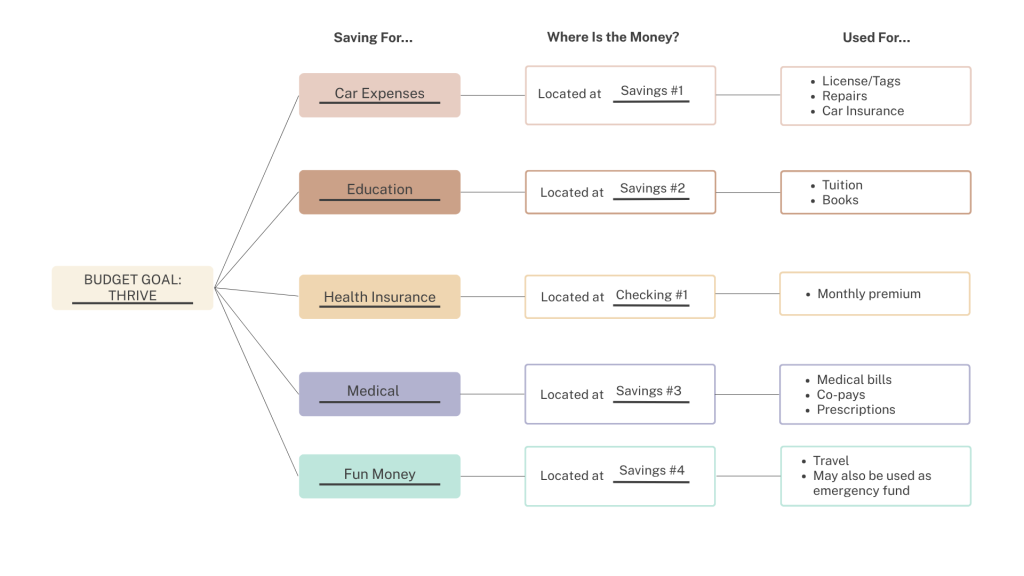

A budget is simply the creation of pools of money. This keeps the total of your funds in front of your eyes regularly.

When I was creating a budget for myself, I had to determine my goal. At the time, I needed a budget that helped me thrive as I was in college. I created pools of money related to commuting back and forth to college, college expenses like tuition and books, among other things. I set up multiple accounts at a credit union, where each account was for a different fund.

Each paycheck, funds were direct deposited to various accounts through payroll. I never ran the risk of overspending this way. I ensured I did not live paycheck to paycheck as long as I stuck to the budget I created.

How to Create Your Own Budget

- Step One: What is your goal?

Write it down. For many people, we have found it is gaining control over their finances. Without a goal in mind, you drive aimlessly with no destination in sight.

- Step Two: What are you saving for?

Create funds that reflect your needs. Examples could include an emergency fund, mortgage payment or rent, car repair, and so on.

- Step Three: Set up savings accounts, each dedicated to a different fund.

Use the money in those various accounts only for that particular fund.

- Step Four: Stay disciplined.

In college, I struggled with staying disciplined and keeping to my budget some days. It is not easy to see the pictures on Facebook or Instagram of the trips friends took during the year and not book trips for yourself! I fought “shiny object syndrome” regularly all through college, but I reminded myself that the day to treat myself would come.

You don’t have to live paycheck to paycheck. You can get control of your finances. All it takes is the right tool — a budget — and the discipline to see it through.

Download our budget PDF to gain control over your finances TODAY!

{kind=link}